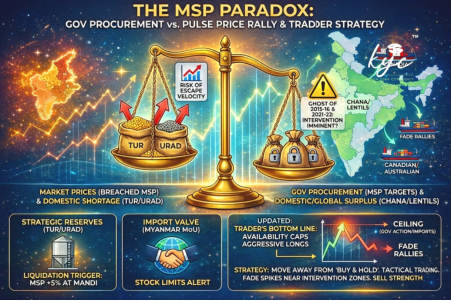

We are facing a million-dollar question in the Indian grains complex: With all pulses (excluding Moong and Masoor) breaching Minimum Support Prices (MSP), can the government realistically meet its procurement targets? At current valuations, the math doesn't look feasible. But if history has taught us anything, it’s that the government—haunted by the ghosts of the 2015-16 and 2021-22 price spikes—will not remain a passive observer. The Supply Matrix: A Complex Basket 🧺 The domestic crop outlook is a study in contrasts: Tur & Urad: Domestic crop looks short compared to last year. Chana: Expecting a bumper crop domestically. Lentils (Masoor): Downside is limited, but the market is heavy with huge crops from Canada and Australia (who also hold significant Chana supply). The Government’s Playbook 🏛️ The administration has managed the pulses complex deftly over the last two years. Expect a multi-pronged strategy to manage this volatility: 1. The "Goldilocks" Target For Tur, the government’s best-case scenario for procurement is a market price 5-8% below MSP. However, with prices currently elevated, they will likely deploy strategic reserves. Trigger: If Mandi prices for Tur sustain 5% above MSP, expect aggressive liquidation of government stocks to cool the rally. 2. The Chana Ceiling While a bumper crop is expected, the government will not tolerate "escape velocity" in Chana

prices. They will anticipate a natural correction as Indian crop arrivals hit the terminal markets, but will intervene if speculation drives prices too high too fast. 3. The Import Valve (Myanmar MoU) The 5-year MoU with Myanmar is already in the works to secure Tur and Urad supply. This is a critical buffer. Watchout: For Urad, if Myanmar exporters attempt to squeeze the market, expect stock limits to be triggered sooner rather than later. 4. Lentils Strategy Given the global supply glut (Canada/Australia), the government might surprisingly be keen on price improvement here to prevent a collapse that hurts domestic farmer sentiment. The Trader’s Bottom Line 📉 The supply side remains steady, but the "shortage psychology" in Tur/Urad is clashing with the "abundance reality" in Chana/Lentils. Actionable View: Tur: Watch the MSP +5% level. That is the intervention zone. Urad: Monitor Myanmar export flows; policy risk (stock limits) is high. Spread Strategy: The "shortage psychology" in specific crops is now colliding with a broader reality: overall availability is sufficient to cap runaway rallies. The trade is no longer a simple "long pulses" play. Availability will not let aggressive longs hold for long. As arrivals pick up, the market will react to the physical flow, but do not fight the government's resolve to cap inflation.