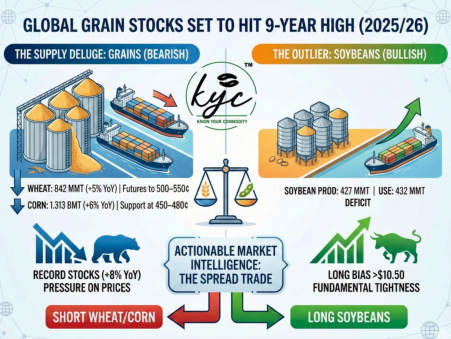

The supply narrative has shifted. The International Grains Council (IGC) just confirmed what the bears have been watching: we are entering a cycle of abundance. Global grain carryover stocks are forecast to hit 634 million tonnes—the highest level in nine years. The Supply Deluge 📉 Total output is projected at a record 2.461 billion tonnes (+6% YoY). Wheat: Hitting a record 842 MMT (+5% YoY) thanks to gains in Canada and Argentina. Corn: Surging to an all-time high of 1.313 billion tonnes (+6% YoY), fueled by massive yields in the US and China. The Disconnect While consumption is climbing to 2.416 billion tonnes, it is lagging behind production speed. The result? Stocks are expanding by 8% year-on-year, the fastest pace of accumulation since 2017/18. The Outlier: Soybeans 🌱 While the grain bins are overflowing, the oilseed complex tells a different story. Soybean production is edging down (427 MMT) against rising consumption (432 MMT). We are looking at a fundamental deficit. Actionable Market Intelligence The IGC Price Index is already down 4% to 213. Here is how to play the divergence: Bearish View (Grains)🐻

The 634 MMT inventory wall creates a heavy ceiling. Wheat: Expect CBOT futures to test the 500–550 cents/bushel range. Corn: Support likely heavily tested at 450–480 cents. Watch Item: Argentina’s exports will bring stiff competition to Black Sea flows. Bullish View (Soybeans)🐂 With use outstripping supply, the fundamental tightness supports a long bias above $10.50/bushel. The Trade: The macro setup favors spread trading. Short Wheat/Corn vs. Long Soybeans.